If you’re looking for a secure investment for your money, term deposits might be a great option for you. Here, we’ll dive into what term deposits are, how they work, and much more.

9 min read

With interest rates on the rise, many of us are looking for ways to grow our savings. However, traditional savings accounts may not always offer optimal interest rates, and options like stocks can involve a lot of risk. For those looking for a happy medium, there’s another financial product to consider: a term deposit account.With a term deposit, you can invest a sum of money into an account for a certain period of time in exchange for a high interest rate payment. They’re a great option for anyone looking to save up for a bigger purchase like a car or home repairs, or to simply grow your savings. But how do term deposits work? And what are the benefits — and downsides — for customers? We’ll dig into all this and more here.

What is a term deposit?

A term deposit is a type of investment where customers transfer a sum of money into a separate account for a fixed period of time in order to earn a set interest rate. Banks offer term deposit accounts to incentivize customers to hold a certain amount of money with them, which the banks then lend out to other customers or businesses. In return, they offer customers a favorable return on their deposit. The time period and interest rate for a term deposit account is agreed upon by the customer and bank. Deposit amounts may vary, and terms can last as little as one month or up to a maximum of 10 years, usually. Once the money is added to the account, the customer can’t access it until the contract ends.

N26 Smart—spend and save with confidence

Discover N26 Smart, our newest premium bank account

What’s the difference between a savings account and a term deposit account?

Standard savings accounts and interest-bearing checking accounts allow customers to set money aside, earn interest on it, and access it as they wish. However, the interest rate on these types of accounts is variable, so it fluctuates depending on market conditions. This means that if interest rates are high, customers will earn a good return. If they’re low, however, customers may not earn any interest at all. Fixed-term deposit accounts, on the other hand, have a predetermined interest rate for the entire period that the money is in the account. So, when a customer deposits their money, they’re guaranteed a concrete return on their investment. This makes term deposit accounts an attractive solution for those who want to earn more bang for their buck, without putting their funds at risk.

Pros of a term deposit account

Term deposit accounts have their share of advantages. For starters, they offer fixed, guaranteed interest rates. This means that, unlike a savings or a brokerage account, you can place your money in the account and know exactly what you’ll earn on your investment. Minimum deposits are generally low, and the terms are flexible — meaning you decide how much money you place in the account and how long it stays there. They’re also a very safe bet. Because most countries have a deposit protection scheme, your money — and the interest it earns — is protected every step of the way. For example, the European Union has a deposit protection scheme that secures your money up to €100,000. And, since the money is safely locked away, you won’t be tempted to go on a spending spree with your savings. Plus, unlike long-term retirement accounts, term deposit accounts don’t require you to lock away your money for long periods of time. Your funds will accrue interest for however long your contract is. When the term is up, you can renew the contract or withdraw the money.

Cons of a term deposit account

Because term deposit accounts keep your savings locked away for a fixed amount of time, one disadvantage of this type of investment is that you won’t be able to withdraw the funds without paying a penalty. Therefore, it’s not a good idea to lock money away in a term deposit account if you might need it soon.Term deposits may also offer lower interest rates compared to other types of securities like stocks or bonds — though they’re also less risky. Like all investments, it can be a gamble. How much your money is working for you depends on a variety of factors, including the fluctuation of interest rates, inflation, and the duration of your term deposit. For example, if interest rates rise significantly while your money is in a term deposit account, you may lose out on that extra interest. However, if they fall substantially, you’ll be earning a comparatively good rate of interest on your deposit.

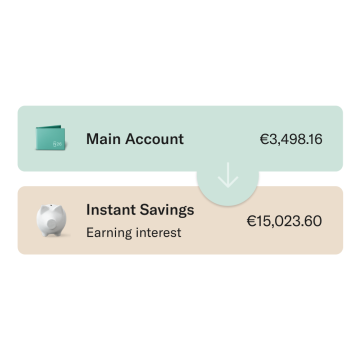

N26 Instant Savings

Earn interest on all your savings and instantly withdraw anytime — with no conditions

To understand how term deposits work, it’s worth looking at how banks do their business. When customers place their money in a savings account, the bank is able to use those funds for lending to other customers. However, if customers are free to withdraw the money in their account whenever they want, banks have a hard time assessing how much money they have at a given time to lend out. To compensate for this, banks incentivize customers to put their money into fixed-term deposit accounts. This gives banks a clearer picture of how much money they’re holding and for how long. In return, they offer customers an attractive interest rate. This way, banks can get the security of having sufficient funds to lend out so that they can earn money, while customers benefit from a comfortable return on their investment.

Investing in fixed-term deposits

To invest in a term deposit, you’ll need to get in touch with your bank to see what options are available. Some banks allow you to invest online and even offer calculators to show you how much interest you’ll earn over different time periods. Then, you just need to decide on your deposit amount and how long you want to keep your funds there. The more money you invest, and the longer you wait, the higher your return will be. Once your deposit is mature — or, in other words, when the contract period is up — you’ll have the option to either withdraw your money or renew the term deposit.

Where can I open a term deposit account?

Most large and midsize banks offer term deposits to their customers. Because interest rates are based on market conditions, you may find comparable offers from different financial institutions. However, it’s worth shopping around to find an account that suits your needs — the terms, conditions, and returns can differ from bank to bank.

What taxes and fees do I have to pay?

With term deposit accounts, you’ll owe taxes on the interest you accrue. These will differ from country to country. In Germany, for example, interest is taxed at a flat rate of 25%, plus a 5.5% solidarity surcharge (26.375% in total, plus church tax if applicable). However, a yearly saver’s tax allowance of €1,000 applies, so you don’t pay capital gains tax up to this amount. The capital gains tax will generally be withheld automatically from your payout once your investment has matured.

Fixed deposit interest rates

As we’ve explained, one of the attractive features of term deposits is their fixed interest rates. They’re especially good when interest rates are high, as it gives customers a secure place to park any savings they’d like to grow. When interest rates are lower, however, customers are incentivized to take on debt at a cheaper price to stimulate the economy — meaning the returns on a term deposit will be comparatively low.

Term deposits in Europe

Interest rates in Europe are set by the European Central Bank (ECB). After a long period of very low interest rates in Europe, the ECB has been progressively raising its interest rates since July 2022. This means that Europeans are now especially incentivized to keep their savings in high-yield accounts like term deposits. Within the EU, term deposit interest rates can vary. That’s because, although interest rates are set by the ECB, there are other factors that cause slight variation between countries, from monetary policy to banking regulations. In Germany, as of October 2023, banks offer anywhere from 0.0-4.25% on deposits for up to 120 months. In France, rates for the same timeframe are up to 4.20%.

Should I invest in fixed-term deposits now?

As you can see, putting your money into a term deposit account has many advantages — and some downsides, too. Here are a few questions to ask yourself if you’re thinking about opening a term deposit account:

Can I afford to not have access to these funds? Remember: You won’t be able to withdraw your money without a penalty, so it’s wise to have a separate emergency fund and a solid budget in place before committing.

What are my short- and long-term savings goals?Having a plan for the future — whether it’s for the next month or the next year — can help you decide how and where to invest your savings. After all, you’ll need to treat your retirement savings differently than, say, funds you want to invest to buy a home one day.

What’s the current economic climate like? Informing yourself about current interest rate fluctuations and market conditions can help you make smarter decisions. For example, you might want to save your money in a term deposit account, or you could be better off applying for a loan to purchase a home.

What’s my risk tolerance? Personality, age, and financial situation all contribute to how much volatility someone can handle. For example, a younger person without too many financial responsibilities might benefit from investing in stocks that have time to grow in value, while those who are older or have less financial stability may prefer a safer investment option.

Budgeting made easy

Visualize your daily expenses and savings to help you make the most out of your money.

No matter what you’re saving for, N26 is the mobile bank that puts you in the driver’s seat. Our savings accountwith smart budgeting tools like Insights and Monthly Wrap-Up allow you to review your finances at a glance, so you can see if you’re on track to meet your goals. Speaking of goals, with our premium Smart, You, and Metal accounts, you can access 10 Spaces sub-accounts to set funds aside for whatever dreams or savings objectives you’re plotting. To save even faster, use Income Sorter or Rules to send a portion of your earnings right into your savings. If you’ve got funds to spare, explore N26 Crypto and buy or sell nearly 200 coins right in your N26 app. Don’t wait a minute longer — sign up for an account today.

Budgeting for the family can feel like a chore, but with a few simple adjustments, it can also be empowering! Read on to discover how to create a family budget the easy way.

Budgeting for the family can feel like a chore, but with a few simple adjustments, it can also be empowering! Read on to discover how to create a family budget the easy way.