Savings accounts, explained: Learn about interest rates, taxes, and more

Are you interested in opening a savings account? Read on to learn everything you need to know to help your money grow.

15 min read

There’s a huge amount of financial products on the market these days to help you save. It’s hard to sift through all the possibilities. In this article, we’ll dive into one of the simplest, most common products out there: savings accounts. Read on to learn what a savings account is, how it works, and the pros and cons of opening one.

What is a savings account?

First things first: in case you aren’t familiar with savings accounts, let’s talk briefly about what they are. As the name suggests, a savings account is an account with a financial institution where you can save your money and earn interest on it. In general, savings accounts refer to either a money market account (Tagesgeldkonto in German) or a fixed-term deposit account (Festgeldkonto).Unlike a normal checking account where you can deposit, spend, and withdraw your money as needed, savings accounts allow you to earn interest on your balance at either a fixed or variable rate. In certain savings accounts, you’ll be able to withdraw your money immediately, or within a matter of days. In fixed-term accounts, however, your funds will be locked away for an agreed-upon time period — usually anywhere from several months to several years. In this guide, we’ll look at why flexible savings accounts can help you save money and increase your financial security. Whether you’re looking to build an emergency fund, grow your wealth, or protect your money against rising inflation, an interest-bearing savings account can be a stable, flexible way to do it.

N26 Smart—spend and save with confidence

Discover N26 Smart, our newest premium bank account

A savings account is an important way to set funds aside — and earn interest at the same time. But where’s the best place to open a savings account, and what’s the process like? Luckily, there are plenty of options to choose from. Let’s take a look. One of the quickest ways to open a savings account is with an online bank. In the last few years, online and digital banks have become more established and now offer a range of finance and savings products to choose from. Customers can open accounts from the comfort of their own homes, without heading to a bank branch or waiting in line. If you want to inquire about bank services, you can usually do that via customer support or online chat. In addition to online banks, you can also open a savings account at a traditional bank, although you’ll need to complete the process in person at a branch. The type of bank you choose is really a matter of personal preference and the products you’re interested in.

Is a savings account free?

When it comes to making financial decisions, costs are a major deciding factor. Whether a savings account is free — or not — depends on the kind of financial product and the bank you’re investing with.Some banks and online brokers offer savings accounts for free. Others charge minimal monthly fees — particularly if certain conditions aren’t met. For example, some providers only offer free savings accounts with a minimum balance. Or, they might require you to open a brokerage account at the same time. It’s always important to check the fee structure and terms and conditions before you open an account. This way, you’ll be able to compare different options and find the one that fits you and your financial goals best.

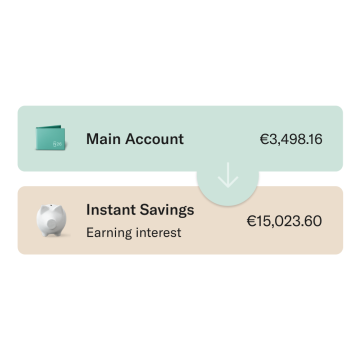

N26 Instant Savings

Earn up to 2.5% interest p.a. with no extra fees, no deposit limits and full flexibility.

How high are interest rates with a savings account?

Because savings accounts allow you to earn interest on your funds, the interest rate is a very important factor when you’re choosing an account. Interest rates can vary quite a bit between banks and products. And new customers often benefit from more attractive interest rates than existing customers do. In the last several months, interest rates have risen dramatically across Europe because of the key interest rate increases by the Central European Bank. However, not every bank has raised their own interest rates accordingly. Another important note: Savings accounts typically have variable interest rates that can change over time, depending on the market. Additionally, the advertised interest rates often only apply to the first six months after the account is opened — and are only for new customers. Make sure you compare accounts at several banks (and read all the fine print!) to figure out which savings account offers the best returns. One option is to use an interest calculator to add up which offers will give you the most bang for your buck. In contrast to flexible savings accounts, fixed-term deposit accounts offer fixed interest rates that remain constant over a certain period of time. That way, you get more certainty and peace of mind. Just note that your funds will probably be locked in for the duration of the contract.

Do I need to pay taxes on the interest I earn in my savings account?

The short answer is: probably. However, the taxes you’ll owe on your interest from a savings account depends on where you live and the country’s tax laws. In Germany, interest income from savings accounts is generally taxable. Since the withholding tax was introduced in 2009, interest income from savings accounts and other capital gains have been taxed at a flat rate. In general, this breaks down to 25%, plus a solidarity surcharge of 5.5% of the withholding tax. When applicable, church tax is also levied on capital gains at a rate of between 8 and 9%. However, this depends on the federal state you live in, and is only calculated on the withholding tax that you incurred. And that’s not all. In Germany, there are certain conditions where you don’t owe capital gains tax. For example, as of 2023, you have an annual allowance of €1,000 if you’re single. If you’re married, you’ll get an allowance of €2,000. This means you won’t have to pay withholding tax on funds earned up to these amounts each year, regardless of whether your capital gains are from share sales, dividends, interest income, or something else. It’s also important that you set up an exemption order with your bank so that they can automatically credit the exemption amount. Regardless of where you live, it’s always a good idea to check the tax regulations for your country and state, as these can change regularly.

Save up with Spaces

Use N26 Spaces sub-accounts to easily organize your money and save up for your goals.

Well, with a savings account, you deposit your money into an account with a financial institution. In return for keeping your funds there, the bank pays you interest on your deposit balance. In essence, you’re receiving financial compensation from the bank for storing your money there. Here’s how the process works: You deposit money into your savings account with the goal of setting it aside and allowing it to grow. For this, you’ll usually receive an IBAN linked to your new account. Unlike a checking account, you can’t use your savings account for everyday purchases, because it doesn’t come with an EC or debit card. How easily and quickly you can withdraw your money depends on the type of savings account you have. With a money market account, for example, you can move money out of your account within a few days. Fixed-term deposit accounts are different. Here, you’ll need to invest your money for a longer period of time. The terms and conditions vary significantly between providers and products, and usually have a minimum commitment of one month.

What documents do you need to open a savings account?

To open a savings account in Germany, you need the following documents: 1. GovernmentID or passport. You’ll need to verify your identity with a valid government ID or passport. The bank needs this document to make sure that you fulfill the legal requirements for opening an account. 2. Tax number. In Germany, submitting your tax number (Steuer ID) is mandatory, as the interest earned on your account is taxable. If you don’t have a tax number, you can request one from your local tax office. 3. Minimum deposit. Some accounts require a minimum deposit, so check with your financial institution to see if this applies.4. Savings account application. The bank will provide you with an application form for you to fill out and sign. You’ll need to enter some personal details and select the type of account you’d like to open.5. Further documentation, if required. Depending on the bank, you may need to provide additional documentation to support your application. As soon as you’ve got all your materials together, the bank will review your application and set you up with your new account. It’s a good idea to check with your bank on their specific process and required documents, since it can vary.

How do I withdraw money from my savings account?

Withdrawing funds from your savings account isn’t too complicated. But there are a few important steps:1. Open your online bank account. The first step in withdrawing funds is to log into your online account or banking app. If you’re working with a bank branch, you can complete this process in person. 2. Identify yourself. Your bank may need to see documentation to verify your identity. With online banking, you’ll likely just need to log in with your username and password (or use two-factor identification), while in a bank branch, you’ll have to show some sort of government-issued ID. 3. Choose your payment method: You can choose how you want to receive your funds. The most common methods are as follows:

Transfer to your checking account

Cash withdrawal (only possible at a bank branch)

Checks (some banks offer the option to issue a check that you can then deposit or cash)

Note that your bank may charge a withdrawal fee, especially if you’ve exceeded the number of transactions allowed per month. So, again, make sure you familiarize yourself with the terms and conditions before you decide to withdraw funds.Additionally, the amount of time it takes to withdraw money from a savings account can vary a lot. With some providers, your funds will be available immediately, while some take several days to process your request.

How much money can I have in my savings account?

In general, there aren’t laws that set a maximum limit for the balance in a savings account. Plus, most providers don’t have a maximum deposit, which means there are no limits to how much money you can put into the savings account. However, some providers have a maximum limit for interest-bearing credit. This means that any amount above the limit won’t earn interest.Some savings accounts, while they have no balance limit, may have limits on deposits. You may only be able to deposit up to a certain amount per month or per year. However, in many cases, these restrictions are relatively low and shouldn’t pose a problem for most investors. One more thing: if you open a savings account that’s protected under the German Deposit Protection Scheme, note that any balance over €100,000 isn’t protected under this law. This means that your funds would be at risk in the event of a banking crisis or market crash.

Passbooks and savings accounts: What’s the difference?

The main difference between a passbook and a savings account is the way they’re managed. Let’s take a look at the differences.

Passbooks: A passbook is a physical ledger typically issued by brick-and-mortar banks. Deposits and withdrawals are entered manually into the book’s pages. This used to be a common way to save money. These types of accounts usually offer lower interest rates compared to other interest-bearing accounts, and you often don’t have access to the entire balance without being charged interest. In today’s digital era, passbooks are less common because they’re less flexible and offer lower interest rates. Some banks have done away with passbooks altogether and offer a savings card or savings account instead.

Savings accounts: A savings account is a modern account offered by traditional financial institutions and online banks. Unlike passbooks, savings account transactions typically occur electronically via online banking or ATMs. Savings accounts often offer higher interest rates than passbooks and allow easier access to money. You can usually transfer or withdraw money from a savings account whenever you want without having to keep a physical ledger. The flexibility and online access make this approach more popular these days.

What’s better: a passbook or a savings account?

The decision of whether to open a passbook account or a savings account depends on your needs and preferences. To help you decide, here’s a list of some advantages and disadvantages for each.

Pros and cons of passbooks

Advantages:

Traditional. Passbooks are a familiar method of saving money over the long term, and many people still prefer this option.

Simple to use. A passbook makes it possible to calculate your savings progress and record interest earned, deposits, and withdrawals all in one place. You’re not reliant on a device or internet connection.

Low risk. Passbooks aren’t subject to the market volatility of other products like stocks or crypto.

Disadvantages:

Lower interest. Compared with savings accounts, passbooks offer lower interest rates, meaning your money will grow more slowly than it might otherwise.

Less flexibility. With many financial institutions, you can only withdraw a certain amount each month without incurring additional fees.

Manual management. Every entry in a passbook has to be done by hand, increasing your bookkeeping work.

Pros and cons of savings accounts

Advantages:

Higher interest rates. Savings accounts offer higher interest rates — especially in a financial climate like we’re experiencing in 2023, when rates are high — meaning you can grow your savings more quickly.

Easy access. Many providers allow you to deposit or withdraw your money whenever you want.

Digital management. Savings accounts allow you to manage your money and make transactions online. With mobile banks, you can even use an app on your smartphone.

Disadvantages:

(Mostly) digital. If you prefer to have a paper trail for every transaction, a savings account might not be the best fit.

Potential fees. Some savings accounts charge fees or offer low interest rates when you don’t meet certain conditions. Some even have monthly fees.

Does it make sense to open a savings account?

Whether a savings account makes sense for you depends on your individual financial goals, your current financial situation, and your personal preferences.If you want to build an emergency fund for unexpected expenses, a savings account can be a good place to put your reserves. You can set up a standing order at many banks to regularly contribute to your emergency fund. Plus, if worse comes to worst, you can get your money quickly.A savings account can also be handy for setting aside money for short-term financial goals, like a new car or a vacation. The interest rates are lower than other forms of investment such as fixed-term deposit accounts, but the money is easily accessible when you need it.If you’re looking for an investment option for your long-term financial goals such as purchasing a home, raising children, or retiring, other forms of investment may be more suitable, like stocks, ETFs, or bonds. These generally offer higher potential returns, although they can also involve higher risks. However, a savings account can be a practical option for storing your cash reserves that you intend to invest, because you can earn interest in the meantime and still have flexible access to your money.

How do I close my savings account?

Sometimes, a savings account is the right choice for a certain period of time — but not forever. If you need to close your savings account, here’s how to do it: 1. Check the cancellation conditions. Each bank has its own rules for closing savings accounts. It’s important to review the termination conditions and any possible fees that may be associated with closing the account. Some savings accounts may have a notice period, while others can be canceled immediately.2. Contact your bank. Next, you’ll need to get in touch with your bank to get the process going. This can usually be done over the phone, online via your online banking portal, or in person at a local bank branch.3. Transfer the funds. Make sure your savings account is balanced before canceling. You can transfer the remaining balance to another account yourself or have it transferred through the bank — some banks offer options for this.4. Confirm the account closure. After you request the account closure, your bank will usually send you written confirmation by email or post. This will include the details of the cancellation and the account balance at the time of closure. After termination, your savings account will be closed and you won’t have access to it anymore. Make sure you keep all the necessary forms and documents, in case you need them later (for example, for your tax return).It's important to note that some savings accounts may charge early termination penalties or withhold interest that has already been earned. Consider the terms and possible financial implications carefully before canceling your savings account.

Budgeting made easy

Visualize your daily expenses and savings to help you make the most out of your money.

When it comes to savings, you know best what to do with your money. That’s why we offer a 100% mobile banking experience that puts you in the driver’s seat. With the N26 app, you’ll enjoy a fully modern banking experience that makes saving easy as 1-2-3. Our premium accounts like N26 Smart offer up to 10 Spaces sub-accounts — virtual piggy banks where you can save for what matters most. Assign them their own IBANs to transfer money in and out — perfect for managing rent, planning vacations, and much more. Ready for a banking experience you’ll truly love? Compare our accounts, and find the one that fits your lifestyle today.

Budgeting for the family can feel like a chore, but with a few simple adjustments, it can also be empowering! Read on to discover how to create a family budget the easy way.

Budgeting for the family can feel like a chore, but with a few simple adjustments, it can also be empowering! Read on to discover how to create a family budget the easy way.