Saving for a big purchase? Here’s how to set yourself up for success

Saving for something big can be both challenging and rewarding. Here’s how to save smart and reach your ambitious savings goal.

5 min read

When it comes to savings goals, the new year often brings a renewed sense of ambition and motivation. Whether your new year’s resolutions are to upgrade your kitchen, buy a van, or plan a big trip, now is a great time to start saving. Saving for a large purchase takes some planning, but anything is possible when you break it down into small, bite-sized chunks. Here’s our step-by-step guide to saving for a large purchase — let’s jump in!

1. Estimate how much you need to save

First things first: Estimate how much money you need to reach your goal. When it comes to saving for a large purchase, this can be quite research-intensive, since there’s often a broad range of items or experiences to choose from — each with a different price tag. Whether you’re saving for a downpayment on a house, a big trip, or further education, get specific about your goal. This will help you narrow down your price range. And when in doubt, budget for slightly more than you think you’ll need. It’s much better to overshoot your target than miss it!

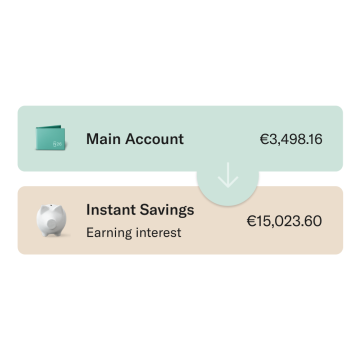

N26 Instant Savings

Earn interest on all your savings and instantly withdraw anytime — with no conditions

Although saving for a large purchase can be exciting, it’s important not to overlook your other financial goals. Ideally, it’s important to hit a few other key financial milestones before you start saving for a big ticket item. These include:

Becoming debt-free. If you have outstanding debts, they’re often incurring interest —meaning that the debt is growing and you’re ultimately losing money. It’s usually best to deal with debt first before starting to save. If you don’t know where to start, check out the debt snowball and debt avalanche budgeting methods.

Building an emergency fund. Living paycheck to paycheck is a reality for many people, but that means there’s no buffer for when a crisis hits. This puts us at financial risk. Before making any short- or long-term savings goals, focus on building up an emergency fund first. This should be between three and six months’ worth of your salary after tax.

Saving for your pension. Saving for the far-off future can seem less fun than buying something you’ve been coveting, but making monthly retirement contributions helps to secure your financial future. You’ll thank yourself later!

3. Get to grips with budgeting

Once you know how much you need to save, the next step is figuring out how much you can realistically contribute towards your savings goal each month. To do this, you need to get to grips with budgeting. The first step to creating a budget is to get familiar with how much money leaves and enters your bank account each month. Then, you can see what you’re actually working with. The simplest way to do this is to get your last three bank statements and make lists of:

All of your incoming money (salary, any other income)

Your outgoing expenses, split into:

Fixed expenses (i.e. essential costs such as rent and bills)

Variable expenses (i.e. non-essential costs such as memberships, meals out, and shopping)

Not only does this give you a solid insight into your financial health, but it highlights areas where you might be overspending and where you could potentially cut back.

Save up with Spaces

Use N26 Spaces sub-accounts to easily organize your money and save up for your goals.

Once you understand the status quo of your money, it’s time to start budgeting. One of the simplest budgets for beginners is the 50/30/20 budgeting method. This approach breaks down your income into three parts:

50% of your income is contributed towards your fixed expenses.

30% is contributed towards your variable expenses.

20% goes towards your saving goals.

Using the 50/30/20 method, you have up to 20% of your income to put toward a savings goal — and that can add up quickly!

4. Set a realistic time limit

After you figure out how much you need to save and how much you can comfortably contribute towards your savings goal each month, you can set a realistic time limit. Simply divide your savings goal by the amount you plan to save each month, and you’ll have an idea of how many months it’ll take to reach your goal.It’s important to set yourself a time limit — it gives focus and urgency to your goal. And it’s good to challenge yourself, as this can make saving feel more rewarding and motivating. But be careful that your timeline isn’t overly ambitious, because that can quickly get discouraging! Try to find a sweet spot where you’re on the edge of your savings comfort zone, but not feeling overwhelmed by unrealistic targets.

5. Set yourself up for success with simple saving hacks

One of the simplest ways to reach your savings goals? Set up a dedicated savings account. By separating your savings from your daily checking account, you significantly reduce the risk of dipping into your savings. Plus, you can clearly watch as your savings fund grows! Once you’ve set up your separate account, it’s time to automate your monthly savings contributions. This means your bank automatically transfers a set amount of money into your savings account each month — and you don’t even have to think about it. By “paying yourself first,” it’s easier not to overspend, blow your budget, or forgo your monthly savings contributions.

Budgeting made easy

Visualize your daily expenses and savings to help you make the most out of your money.

Working toward a special savings goal can be rewarding in more ways than one. N26’s Spaces sub-accounts are like virtual piggy banks—dedicated places where you can tuck your money safely away and watch your savings grow. Plus, as a savings account, N26 offers built-in budgeting tools and smart features to help you get more out of your money. Check out our accounts today and get one step closer to reaching your savings goals.

Budgeting for the family can feel like a chore, but with a few simple adjustments, it can also be empowering! Read on to discover how to create a family budget the easy way.

Budgeting for the family can feel like a chore, but with a few simple adjustments, it can also be empowering! Read on to discover how to create a family budget the easy way.