The 50/30/20 rule: how to budget your money more efficiently

The 50/30/20 budget is beautiful in its simplicity. It can help you divide your income into categories that make saving easy.

8 min read

Budgeting doesn’t need to be complicated, nor should it take hours out of your day. In fact, the best ways to budget are often the simplest. Take, for example, the 50/30/20 rule. The 50/30/20 rule is a straightforward monthly budgeting method that tells you exactly how much to put towards your savings and your living costs each month.With a clear big-picture overview of your budget for the month, you can confidently avoid overspending and build up your savings over time—all without painstakingly recording every single transaction.So, if you’ve ever downloaded a budgeting app only to abandon it by the third day, you might want to give the 50/30/20 method a try. It’s one of the best budgeting tips we’ve found, and here’s how it works.

What is the 50/30/20 rule?

The 50/30/20 rule is an easy budgeting method that can help you to manage your money effectively, simply and sustainably. The basic rule of thumb is to divide your monthly after-tax income into three spending categories: 50% for needs, 30% for wants and 20% for savings or paying off debt.

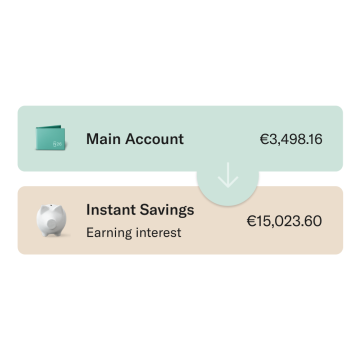

N26 Instant Savings

Earn interest on all your savings and instantly withdraw anytime — with no conditions

By regularly keeping your expenses balanced across these main spending areas, you can put your money to work more efficiently. And with only three major categories to track, you can save yourself the time and stress of digging into the details every time you spend.However, the 50/30/20 rule should only be used as a rule of thumb for budget planning. The exact percentages for each category depend on your personal financial situation, local cost of living, inflation, and many other factors.One question we hear a lot when it comes to budgeting is, “Why can’t I save more?” The 50/30/20 rule is a great way to solve that age-old riddle and build more structure into your spending habits. It can make it easier to reach your financial goals, whether you’re saving up for a rainy day or working to pay off debt.

Where did the 50/30/20 rule come from?

The 50/30/20 rule originates from the 2005 book, “All Your Worth: The Ultimate Lifetime Money Plan,” written by current US Senator Elizabeth Warren and her daughter, Amelia Warren Tyagi.Referencing over 20 years of research, Warren and Tyagi conclude that you don’t need a complicated budget to get your finances in check. All you need to do is balance your money across your needs, wants and savings goals by using the 50/30/20 rule.

Savings Tips | The 50-30-20 Rule

How to budget your money with the 50/30/20 rule

The 50/30/20 rule simplifies budgeting by dividing your after-tax income into just three spending categories: needs, wants and savings or debts. Knowing exactly how much to spend on each category will make it easier to stick to your budget, and help keep your spending in check. Here’s what a budget that adheres to the 50/30/20 rule looks like:

Spend 50% of your money on needs

Simply put, needs are expenses that you can’t avoid—payments for all the essentials that would be difficult to live without. 50% of your after-tax income should cover your most necessary costs.Needs may include:

Monthly rent

Electricity and gas bills

Transportation

Insurances (for healthcare, car, or pets)

Minimum loan repayments

Basic groceries

For example, if your monthly after-tax income is €2000, €1000 should be allocated to your needs.This budget may differ from one person to another. If you find that your needs add up to much more than 50% of your take-home income, you may be able to make some changes to bring those expenses down a bit. This could be as simple as swapping to a different energy provider, or finding some new ways to save money while grocery shopping. It could also mean deeper life changes, such as looking for a less-expensive living situation.

Spend 30% of your money on wants

With 50% of your after-tax income taking care of your most basic needs, 30% of your after-tax income can be used to cover your wants. Wants are defined as non-essential expenses—things that you choose to spend your money on, although you could live without them if you had to. These may include:

Dining out

Clothes shopping

Holidays

Gym membership

Entertainment subscriptions (Netflix, HBO, Amazon Prime)

Groceries (other than the essentials)

Using the same example as above, if your monthly after-tax income is €2000, you can spend €600 for your wants. And if you discover that you’re spending too much on your wants, it’s worth thinking about which of those you could cut back on. As a side note, following the 50/30/20 rule doesn’t mean not being able to enjoy your life. It simply means being more conscious about your money by finding areas in your budget where you’re needlessly overspending. If you’re confused about whether something is a need or a want, simply ask yourself, “Could I live without this?” If the answer is yes, that’s probably a want.

Stash 20% of your money for savings

With 50% of your monthly income going towards your needs and 30% allocated to your wants, the remaining 20% can be put towards achieving your savings goals, or paying back any outstanding debts. Although minimum repayments are considered needs, any extra repayments reduce your existing debt and future interest, so they are classified as savings.Consistently putting aside 20% of your pay each month can help you build a better, more durable savings plan. This is true whether your ultimate goal is building an emergency fund, developing a long-term personal financial plan, or even preparing for a down payment on a house.And it’s impressive how quickly the savings can add up. If you bring home €2000 after tax each month, you could put €400 towards your savings goals. In just a year, you’ll have saved close to €5000!

Save up with Spaces

Use N26 Spaces sub-accounts to easily organize your money and save up for your goals.

How to apply the 50/30/20 rule: a step-by-step guide

So, how do you actually use the 50/30/20 rule? To put this simple budgeting rule into action, you’ll have to calculate the 50/30/20 ratio based on your income and categorize your spending. Here’s how:

1. Calculate your after-tax income

The first step to using the 50/30/20 budgeting rule is to calculate your after-tax income. If you’re a freelancer, your after-tax income will be what you earn in a month, minus your business expenses and the amount you’ve set aside for taxes. If you’re an employee with a steady paycheck, this will be easier. Take a look at your payslip to see how much lands in your bank account each month. If your paycheck automatically deducts payments such as health insurance or pension funds, add them back in.

2. Categorize your spending for the past month

To get a true picture of where your money goes each month, you’ll need to see how and where you’ve spent your income over the past month. Grab a copy of your bank statement for the past 30 days, or simply use the Insights feature in your N26 app. It automatically sorts all your transactions into categories such as Salary, Food & Groceries, Leisure & Entertainment, and more.Now, split all your expenses into the three categories: needs, wants and savings. Remember, a need is an essential expense that you can’t live without, such as rent. A want is an additional luxury that you could live without, such as dining out. And savings are additional debt repayments, retirement contributions to your pension fund, or money that you’re saving for a rainy day.

3. Evaluate and adjust your spending to match the 50/30/20 rule

Now that you can see how much of your money goes towards your needs, wants and savings each month, you can start to adjust your budget to match the 50/30/20 rule. The best way to do this is to assess how much you spend on your wants every month.According to the 50/30/20 rule, a want is not extravagant—it’s a basic nicety that allows you to enjoy life. As cutting back on your needs can be a complex and challenging task, it’s best to work out which of your wants you can cut back on to stay within 30% of your take-home income. The more you reduce spending on your wants, the more likely it is that you’ll be able to hit your 20% savings target.

50/30/20 rule spreadsheet

While our 50/30/20 rule calculator can provide a general overview of your ideal 50/30/20 rule budget, a 50/30/20 rule spreadsheet is a good option if you’d like to create a more in-depth budget.Spreadsheet software such as Microsoft Excel, Google Sheets and Apple Numbers all offer premade templates to help make spreadsheet budgeting easy. You can find plenty of free online 50/30/20 rule spreadsheets that are compatible with whichever program you’re using.

Budgeting made easy

Visualize your daily expenses and savings to help you make the most out of your money.

Budgeting methods can help you feel more reassured and in control of your financial picture. But it also helps to have financial tools that can help you along the way. At N26, we want to help you reach your budgeting goals without breaking a sweat. Access your money from anywhere with your 100% mobile savings account, and get instant push notifications for an up-to-date picture of your finances. What’s more, your free Spaces sub-accounts can help you track multiple savings goals, while N26 Insights will automatically categorize your spending for you to help you keep on track.

Budgeting for the family can feel like a chore, but with a few simple adjustments, it can also be empowering! Read on to discover how to create a family budget the easy way.

Budgeting for the family can feel like a chore, but with a few simple adjustments, it can also be empowering! Read on to discover how to create a family budget the easy way.