Budgeting doesn’t need to be stressful or confusing. These simple budgeting tips show you how you can start saving today.

8 min read

Although it may seem daunting, working out how to budget your money doesn’t need to be hard. With these practical budgeting tips, saving up for your short- and long-term goals can almost seem effortless. And these tips aren’t just for those with a ton of disposable income. If you’re wondering how to budget money on low income, we’ve got you covered with smart methods such as the 50/30/20 budget rule.Read on to learn about five of our favorite tried-and-true budgeting tips.

1. Don’t ask how to budget money—ask why you want to budget

It may sound simple, but the first step to creating a budget is to determine exactly why you want to start saving money. The key to success in any endeavor is to create specific, yet challenging objectives. Understanding what motivates you to save can go a long way toward creating clear, achievable savings targets. And keeping your savings goals in mind can help you to stay focused and on track, even when things aren’t so easy.Here are three questions you might want to ask yourself before making your budget:

What is important to you? For example, do you live to travel? Do you dream of becoming a homeowner? Or would you like to save up for studying?

What is a realistic, yet challenging, goal that you want to save for?

Is this goal motivating enough that you will want to stick with it, even if there are periods in which saving becomes a little tricky?

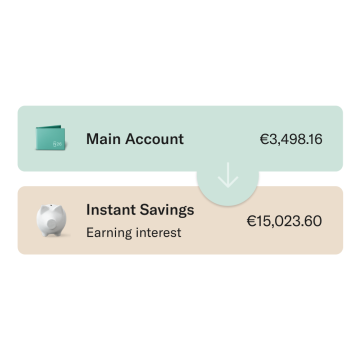

N26 Instant Savings

Earn interest on all your savings and instantly withdraw anytime — with no conditions

2. Distinguish between short-term savings goals and long-term saving goals

Once you’ve asked yourself why you want to start saving, the next step in building a budget is to divide your savings goals into short- and long-term plans.What is a short-term savings goal? These relatively modest targets may include the following:

Having a combination of both short- and long-term saving goals can make the larger goals seem less intimidating. As you gradually achieve your short-term goals, you may realize how possible it is to save money and be in control of your finances. And this can make your long-term goals feel increasingly attainable.

How Can I Save More Money? Tips for Sticking to a Budget | N26

How to budget money realistically

Before starting your budget, consider whether your short- and long-term savings goals are realistic. There’s nothing more demotivating than setting an idealized, yet totally unattainable goal and watching it become increasingly impossible to achieve. A fantastic personal budgeting tip is to follow psychologist Edwin Locke’s SMART goal-setting method. SMART stands for: Specific, Measurable, Attainable, Relevant, and Time-bound. As long as your budgeting goals adhere to each and every one of these five descriptions, they’re realistic enough for you to start your budget.

Save up with Spaces

Use N26 Spaces sub-accounts to easily organize your money and save up for your goals.

If you want to start budgeting effectively, you need to understand exactly how much is coming in and out of your account every month. The best way to do this is to track all of your income and expenses over a 30-day period. This means being aware of every single transaction and either noting it down in a spreadsheet or using a budgeting app such as You Need a Budget.

4. Separate fixed expenses from variable expenses

Once you’ve got a good overview of where all your money is coming and going each month, the next step is to separate your expenditures into fixed and variable costs. The category of fixed costs may include:

Entertainment (i.e. nights out, cinema trips, concerts)

Clothes shopping

Eating out

Personal budgeting tips for reducing your variable costs

While your fixed costs do not offer you much—if any—flexibility with regards to saving, your variable costs do. This doesn’t mean that you have to stop going out and having fun. It just means building everyday habits to help you save a bit more. Here are some budgeting tips you might want to consider to lower your variable costs:

Prep your meals at home instead of going out for lunch at work.

Consider if you really need to upgrade your phone to the latest model if your current model is working just fine.

Choose one day a week where you don’t spend anything on variable costs.

Adopt the save now, spend later technique. This means setting aside your money for your savings goals and fixed costs at the beginning of the month and only using the remaining balance to pay for your monthly variable costs.

5. Plan a monthly budget

So, you’ve worked out why you want to budget, what you want to save for, and what your fixed and variable costs are. Now it’s time to work out how to save money each month.Of course, this varies dramatically from person to person. You may be a freelancer with variable income or a full-time employee with a steady paycheck. Or maybe you’re trying to stretch every last dollar to save on low income. Whatever the case may be, we’ve compiled some smart budgeting tips that can work with any level of income.

N26 Rules and RoundUps - Save money more easily

The 50/20/30 rule

The 50/30/20 rule encourages your budget to look as follows:

50% of your income goes towards your “needs,” i.e. your fixed costs such as rent and bills.

30% is allocated to your “wants,” i.e. your variable costs such as eating out, trips to the hairdresser and clothes shopping.

20% goes into your savings or towards paying off debt.

The 50/30/20 rule was actually created by US senator Elizabeth Warren, a bankruptcy specialist at Harvard, as a way to show American citizens how to budget and save money and how to budget money on a low income. If you decide to opt for the 50/30/20 method, consider automating your expenses each month. This means that your income is automatically divided at the beginning of the month in accordance with the 50/30/20 rule. By doing this, you’ll only be left with the 30% allocated to “wants” in your bank account, which you can then spend during the month without worrying about whether you are overspending or not meeting your budgeting goals.

The zero-based budget

The zero-based budgeting method differs slightly from the 50/30/20 approach in that it looks at assigning each penny a specific job. At the end of the month, all income minus all expenditures should equal zero; there should be no left-over money in your account. This means fine-tuning your budget so that you know exactly how much you are spending on your fixed, variable and savings costs each month, to the cent. This is a very detail-orientated approach to budgeting, and means that you need to be acutely aware of all of your monthly transactions as they happen.

Create a budgeting contingency plan

Life always comes with a few surprises, so it’s a good idea to have a budgeting contingency plan for when things get a little complicated. One of the best budgeting tips is to prepare for when you may not be able to stick so closely to your plan. This stops you from becoming demotivated and losing track of your budgeting goals completely. Here are some tips for creating a contingency plan:

Factor in saving for an emergency fund as part of your budget. This could mean saving five percent of your income every month for those unforeseeable circumstances.

Create a fallback budget which you refer to in an emergency. This budget cuts out everything that isn’t essential for everyday life, i.e. variable costs. This frees up some money to use in an emergency.

Budgeting made easy

Visualize your daily expenses and savings to help you make the most out of your money.

Looking for the perfect way to put all of these budgeting tips into action? With a N26 Smart bank account, you can track each and every transaction by being notified when any money enters or leaves your account. Plus, the Spaces feature allows you to set up several sub-accounts and to assign a savings target to each of them. This means you can keep a close eye on how close you are to reaching your goals.Your financial wellbeing and getting the most out of your money are important. Whether you’re looking for budgeting tips for students, trying to learn the basics of money or saving up for a big investment, making your money work for you is key for a balanced, healthy lifestyle.

Sources:

expertprogrammanagement(Locke’s SMART method) Goal-Setting Theory of Motivation by Fred C. Lunenburg

Budgeting for the family can feel like a chore, but with a few simple adjustments, it can also be empowering! Read on to discover how to create a family budget the easy way.

Budgeting for the family can feel like a chore, but with a few simple adjustments, it can also be empowering! Read on to discover how to create a family budget the easy way.