What is an emergency and rainy day fund? Here’s how to set one up

Give yourself some peace of mind by saving for life’s unexpected surprises.

11 min read

Especially in uncertain times such as this, saving for an emergency fund and a ‘rainy day fund’ is a great way to give yourself some peace of mind for the future. And with so many of us living from paycheck to paycheck—and often having less than a month’s salary saved up in reserves—creating a financial buffer is essential for keeping your budgeting goals on track, and to stop you from getting into debt. But how much should you put into an emergency fund, and what is the difference between this form of saving and a rainy day fund? Let’s find out!

What is an emergency fund?

To put it simply, an emergency fund is a financial safety net that protects you from life’s unexpected events. Instead of having to rely on your bank account’s overdraft, or having to borrow money to help you out in a crisis, you can dip into this designated crisis fund without worrying about the knock-on effect for the rest of your finances.

How to create a rainy day fund

But, what counts as an emergency?

An emergency fund should only be used when something truly unexpected happens, which needs your urgent attention, and that you have no choice but to pay for. Examples of when to use it could include:

If you unexpectedly lose your job and lose your source of income

If you need to pay for sudden medical expenses

If the economy goes into a recession and you lose a significant amount of income

If you suddenly have to relocate to look after an ill relative

How does a rainy day fund differ?

A rainy day fund is similar to an emergency fund, but its function is to pay for life’s smaller surprise expenses. These one-off expenses include covering situations like the following:

Having to purchase a new fridge if your current one breaks down

Vets bills if your cat needs medical attention

Car repair bills

Buying a new phone if your current one gets stolen

While all of these expenses are necessary, they aren’t quite as costly or dramatic as the reasons for dipping into your emergency fund.

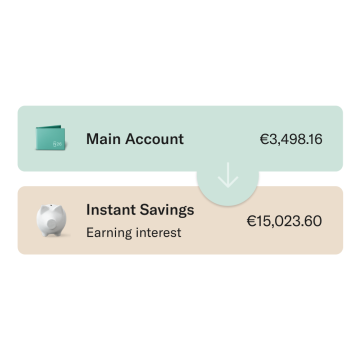

N26 Instant Savings

Earn interest on all your savings and instantly withdraw anytime — with no conditions

When should I budget for an emergency or rainy day fund?

By saving into an emergency and a rainy day fund, you are essentially buying yourself peace of mind for the future. When crisis hits—large or small—your finances won’t add to your stress levels as these will already have been taken care of, so you can get on with what needs to be done.To get ahead and enjoy that extra peace of mind that comes with knowing that you’ve got money stashed away, it’s best to move money over whenever you can—or at least once a month to maintain some sort of cash flow.

The benefits of an emergency and a rainy day fund

The advantages of having both an emergency and a rainy day fund are priceless. Here’s why:

You’ll reduce stress, safe in the knowledge that you have a financial safety net.

You’ll develop a money-saving mentality, and preparing for the future is more likely to prevent you from making rash financial decisions in the present.

An emergency fund also protects you from dipping into other savings accounts when a crisis hits, helping you to stay on target with all of your budgeting and saving goals.

How much should I save each month?

Experts estimate that an emergency fund should include around three to six months worth of your fixed monthly living expenses (including rent, insurance fees, gas and electricity bills). While some opt to also include their variable expenses (grocery shopping, money for nights-out and general entertainment) into the emergency fund budget, it’s more common to focus on ensuring that you have up to six months of your monthly fixed costs stored away in savings.

The amount that you need depends on your lifestyle

Whether you decide to save three or six months of your fixed costs is dependent on your means and current lifestyle. Those who live in one-person households, and those with more unstable revenue streams—such as freelancers—might be safer opting to save for six months. This is because their financial safety net may be a bit thinner than those in a two-person household, where someone else can be a financial support in a crisis, and than those with a more regular source of income.

Rainy day fund––how much should you save?

A rainy day fund should hold enough money to cover you for some of life’s smaller emergencies, but it really depends on your own individual circumstances. While estimates vary between €500 and €2500, if you can, it’s best to err on the side of caution and set aside at least €1000. However, it’s worth considering that while €1000 should be enough to cover things such as replacing a household appliance or paying for a surprise vet bill, it might not be able to cover both of them simultaneously.

Try to predict how much you will need for your rainy day fund

A great way of working out how much you should set aside for your rainy day fund is to try to assess your current situation, then see if you can predict any future expenses. This will give you a clearer idea of whether you should aim to save €500 or more. Such foreseeable circumstances may include:

The cost of car repair if you have a car that is prone to breaking down

Vet bills if you have an older pet

Dental bills if you have a history of requiring frequent dental work

Assessing the age and functionality of your essential appliances, especially those that are no longer covered by any warranty. Once you have a clearer idea of what may constitute your potential smaller surprise expenses down the line, you can reach a better estimate of how much money to budget into your rainy day fund, and then better prepare.

Save up with Spaces

Use N26 Spaces sub-accounts to easily organize your money and save up for your goals.

Start saving for a rainy day fund before saving for an emergency fund

Because your rainy day fund is easier to save for, it’s worth focusing on getting that set aside first before moving on to your emergency fund. You’re more likely to dip into your rainy day fund more often than your crisis fund, since the chances of your fridge breaking down or your plumbing going awry is greater than that of you experiencing a life-changing emergency. Consequently, it’s a good idea to have a buffer for life’s smaller surprises on hand, and it helps keep your emergency savings targets on track.

Here’s how to create an emergency and a rainy day fund

Starting and maintaining an emergency and a rainy day fund may seem daunting at first, but if you follow these steps, it’s actually pretty easy. By including these funds in your monthly budget, saving for them simply becomes a habit. Here’s how to set them up, step-by-step:

Make a budget

The first step to saving for an emergency fund and a rainy day fund is to create a solid budget. By following these stages, you’ll be well on your way to start saving for an emergency:

Track all of your expenses for 30 days, noting down all of your incomings and outgoings.

Make a distinction between your fixed and your variable costs. Your fixed costs are all the costs you have little choice over (rent, debt repayments, car insurance) whereas your variable costs are more flexible (grocery shopping, money spent on nights out, gym membership).

Decide what percentage of your variable costs you could use to contribute monthly towards first, a rainy day fund, and secondly, to an emergency fund. For example, if your income is €3000 a month and your fixed costs are €2000 a month, you’d be left with €1000 a month of variable costs. From here, you might decide to save 25 percent, which would be €250 a month. By the end of the year, you’d have saved €2500, which could constitute your entire rainy day fund plus the beginnings of your emergency fund.

Use an emergency fund calculator

If you’re really struggling to work out how much to set aside in your emergency savings every month, it might be worth considering using an emergency fund calculator. You can easily find these calculators online. These will help you work out exactly how much you’d have left to add into your emergency fund after extracting all of your fixed costs. It is, however, worth finding an emergency fund calculator that allows you to input many variables, since this will give you a more realistic view of how much you can put into your emergency savings each month.

Save something, at least

It’s important not to get disheartened if saving for six months of fixed living costs seems like too great a number. Saving something is always better than nothing.For example, if you manage to save €30 a week, that’s still €1440 a year, which is still a significant amount. Due to their very nature, an emergency might happen tomorrow, or not for ten years. If you continued to save €30 a week for ten years, then you’d still have a substantial €14,400 protecting you from any financial crisis!

Make your savings automatic

Once you’ve set up your budget, it’s a good idea to make saving for your emergency fund automatic. This means setting up a direct debit from your account into your savings account every month so that you don’t even have to think about doing it manually, and you’re less tempted to start spending it.

Adjust your budget monthly

Being flexible with your budget given inevitable shifts in your incomings and outgoings is essential if you want to avoid becoming demotivated.. Every month it’s worth checking if you can really afford to put your budgeted amount into your emergency or rainy day fund. Alternatively, you might be able to put in a bit more than you had anticipated!

Create a fallback budget

An emergency or rainy day fund should only be used in times of necessity, as should a fallback budget. A fallback budget is basically the budget you adhere to when a crisis hits and money becomes more sparse. It covers all of your fixed costs and perhaps enough to cover basic grocery shopping, but nothing else. This means that you spend the very least amount that you can in a month in the hope that your emergency savings fund—plus any extra freed up cash generated by using your fallback budget—can cover the costs of your immediate emergency.

Celebrate your successes

Perhaps the most enjoyable part of saving for an emergency or rainy day fund is rewarding yourself each time you achieve a significant milestone. For example, say you are aiming to create an emergency fund of €6000. Every time you save €1000, perhaps you treat yourself to a special dinner or a trip to the cinema, or you book yourself in for a new haircut. It’s important to make the process enjoyable, as this means you’re more likely to stick to your savings goals.

Where to keep your emergency fund and rainy day fund

Your emergency and rainy day funds should be kept somewhere that you can access easily in a crisis. A digital bank with a debit card, or a designated are ideal, as you can withdraw money easily, wherever you are. It’s also important that you keep your emergency and rainy day funds separate from each other and from your daily savings account, as you don’t want to be easily tempted to dip into them.

Quick ways to add to your rainy day fund jar and boost your emergency fund

Like most things that are worth doing, beginning is nearly always the hardest part. However, saving money may be easier than you think. If you’re struggling to get the ball rolling with your rainy day and emergency saving goals, here are some excellent ways to free up some extra cash to give yourself a head start:

Put any tax rebates, work bonuses, or money you’ve received as a gift straight into your savings funds.

Free up some extra money and declutter your home simultaneously by selling any unused items online.

Consider taking up a side gig or putting in a few extra hours at work, then using this extra cash to boost your emergency or rainy day funds.

Attempt a no-spend month, or if that’s too difficult, nominate one day per week where you spend nothing (with the exemption of your necessary fixed costs, of course!).

Budgeting made easy

Visualize your daily expenses and savings to help you make the most out of your money.

With N26 , saving for your emergency and rainy day funds couldn’t be easier. Thanks to Spaces, you can create sub-accounts which show you how close you are to achieving your savings goals. And with Statistics giving you a better overview of your monthly income and expenditure, budgeting can become even easier, helping you create better financial habits. Want to learn more about how to budget? Then check out our budgeting how-to guide and start putting a little extra aside to buffer you against the surprises of tomorrow, today.